The Name Is Bond, High Yield Bond

The Name Is Bond, High Yield Bond

Reving up the ole blog again. Excuse the inconsistency, I need inspiration to write this thing and I don’t really choose when that hits (although it usually happens when I am in the shower at night, which is validated by science). Also, selfishly it’s a lot easier for me to grow my account shitposting a meme that takes 30 seconds to make compared to pouring my heart and soul into some obscure 2,000 essay making obscure Star Wars and Sopranos references about the leverage finance market lol. But the blog followers are a loyal bunch and I’m overdue. Today’s class is in session and we are going to cover some intermediate credit agreement terms.

Credit Agreement Espionage

I like to think that when PE associates start their new gig, they are debriefed similar to a James Bond movie. In it, the VP is the old sassy British chick “M” who walks Bond through all the weapons at his disposal in a private equity firm’s valiant effort to give the Firefighter and Teacher pension funds the top quartile alternative investment returns that they ask for (while accumulating a sliver of carry along the way, of course).

So they’re walking through the standard issue weapons: tear gas(lighting) to be used on lenders, diligence grenandes to lob at unsuspecting management teams and investment bankers, even a samurai sword to cut through the weeds of a dataroom. After describing all the weapons in the room, the associate begins to leave to get to work, when the VP stops him “actually Bond, there’s a couple more items we have to show you. These are highly potent and should only be used in emergencies when our cash equity is at stake. ” He then hits a button that opens up a secret room labeled Credit Agreement Fuckery Tools.

End Scene (unrelated to finance but this topical tweet fucking killed me the other day)

By this point I am assuming everyone knows what a credit agreement is. If you don’t, do some research and come back. I posted the below meme the other day about some more niche credit agreement terms, and wanted to do a deeper dive on each.

While sponsors and lenders generally play nice in the sandbox (as acting out of turn can ruin relationships and corresponding deal flow), when shit hits the fan, sponsors will break the emergency glass and use whatever they can to execute on acquisition strategy, preserve liquidity, etc. You’ve probably seen all the sponsor on lender violence in the news and the below terms are often what allows these things to happen.

Incurrence Test / Ratio Debt: The incurrence test is the max point of leverage the company take their debt up to (excluding some of the carveouts described below). So if leverage is 4.5x and the incurrence test is 5.5x, the Company can lever up to 5.5x with zero questions asked. So a deal could be at 2.0x leverage today with 4.5x leverage pricing and you’d be like “wow great deal sign me up”. BUT when you read the fine print, you see incurrence test leverage is 6.0x. Oof. This is a huge “butt”. I’m talking huge. Like the kind of butt that’d be the result of some sort of cheap frankenstein BBL surgery gone wrong (the sub 10k follower IG model risked going to a cheap doctor she found on groupon and is now paralyzed from the ass down). The incurrence test is tough but fair, and any deal team with a brain is going to structure/price deals off the incurrence test rather than closing leverage to allow the company to pay interest at its max debt load (unless, say interest rates absolutely skyrocket right after some of the most aggressively leveraged loans in history were issued in 2020-2021…)

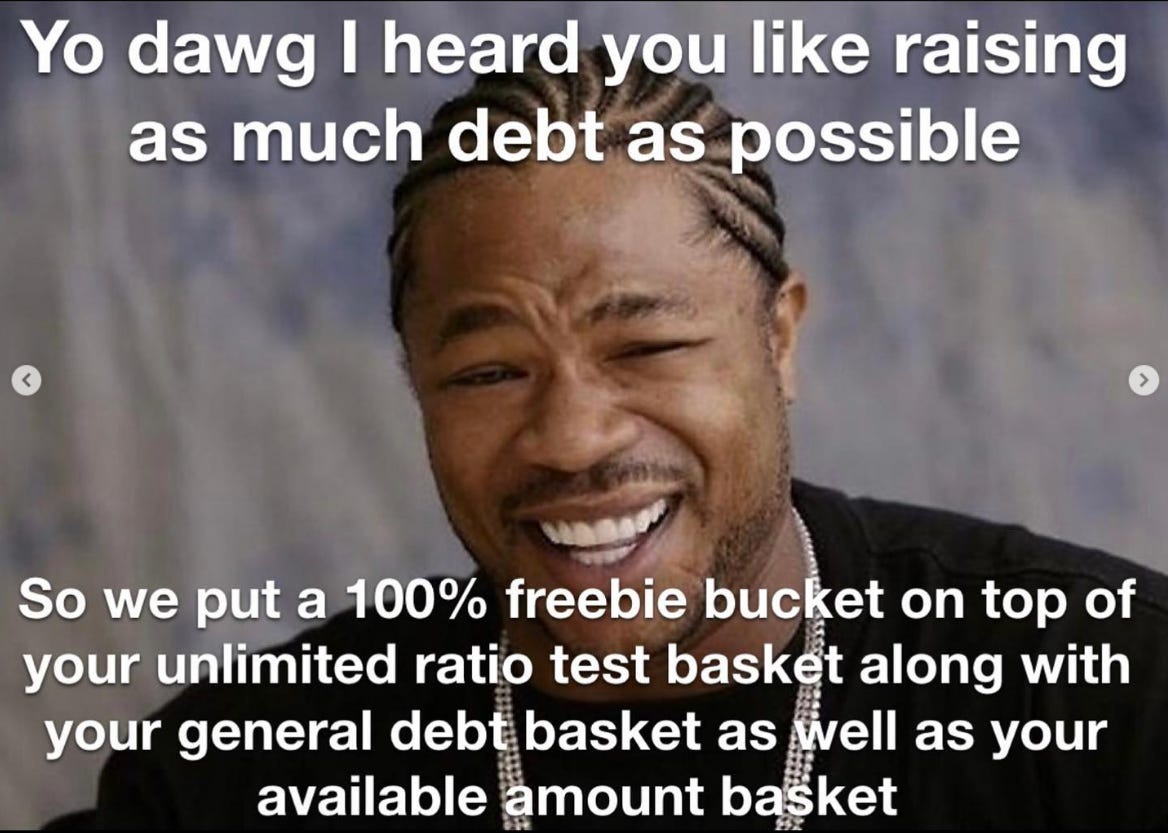

Freebie / Free & Clear Bucket: So lets say the Company levers up to their max incurrence ratio as described above. But the sponsor’s insatiable taste for leverage has not been quenched. That’s where the freebie bucket / Free & Clear (“F&C”) incremental basket comes in. This is one of the most aggressive terms in any credit agreement, and has somehow become widely accepted across the lending universe. It allows for the incurrence of debt ABOVE the max amount allowed under the incurrence test. So if your F&C basket is 100% of EBITDA, you could take your 6.0x incurrence test deal listed above and lever it to 7.0x. Even worse for creditors, borrowers can usually raise this debt outside of their credit agreement. So the sponsor can say “oh, the bank group won’t agree to give me an extra turn of leverage because it will completely fuck the credit profile up? That’s chill, I’ll just go down the street and raise it from a homeless day trader who is thirsty for yield”

Restricted Payments (“RP’s”): The purpose of this bucket is to define how much cash the Company can siphon away from the creditors. RP’s include dividends, junior debt payments, and movement of cash from restricted subsidiaries to unrestricted subsidiaries (once in an unrestricted sub, creditors have no claim to it). This bucket has been used in pretty much every instance of sponsor on lender violence (Jcrew, Chewy, Etc.). Typically structured as an incurrence test like structure (allowed unlimited dividends as long as leverage is below a certain point) but usually also includes a general basket (no leverage governor).

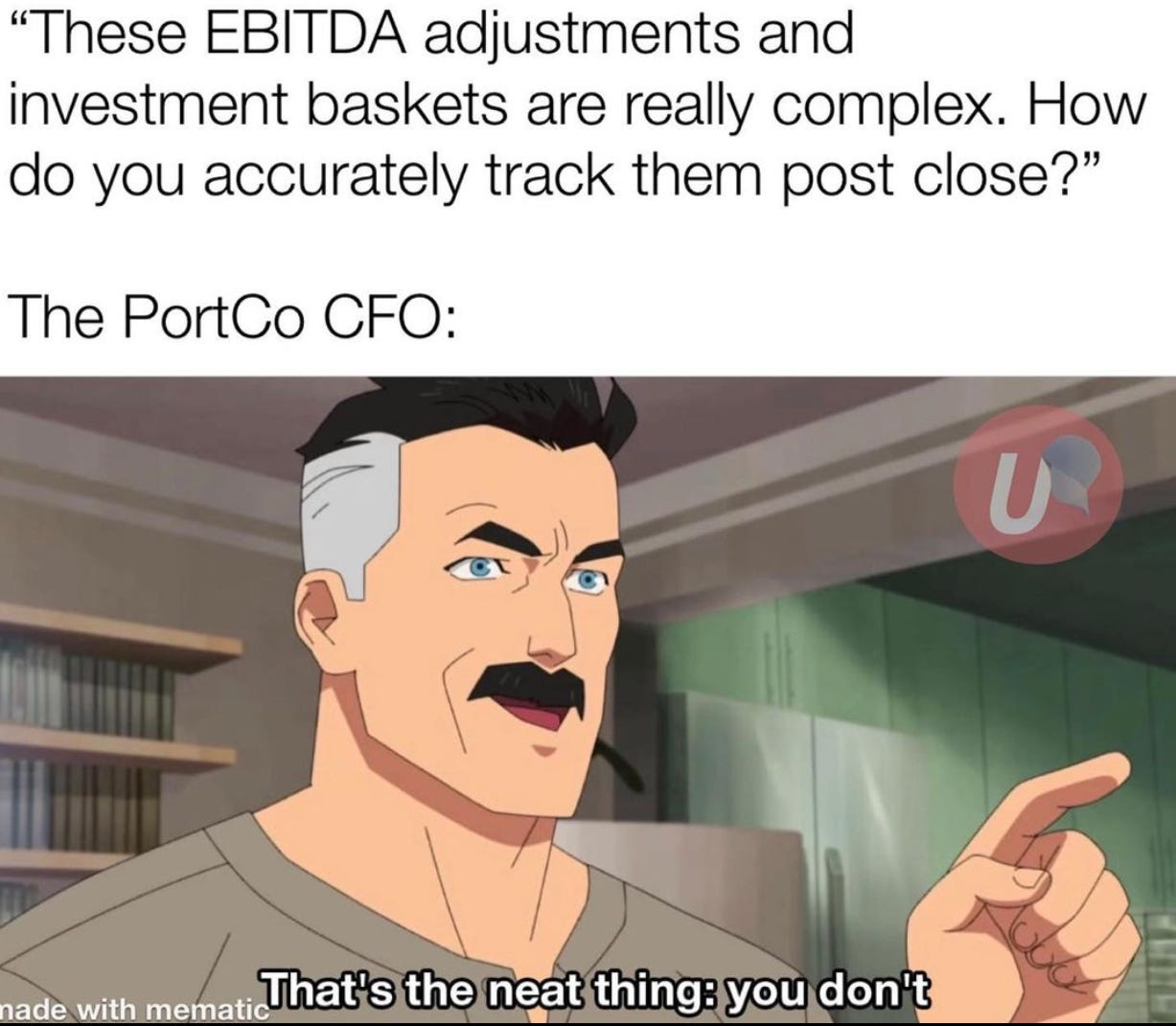

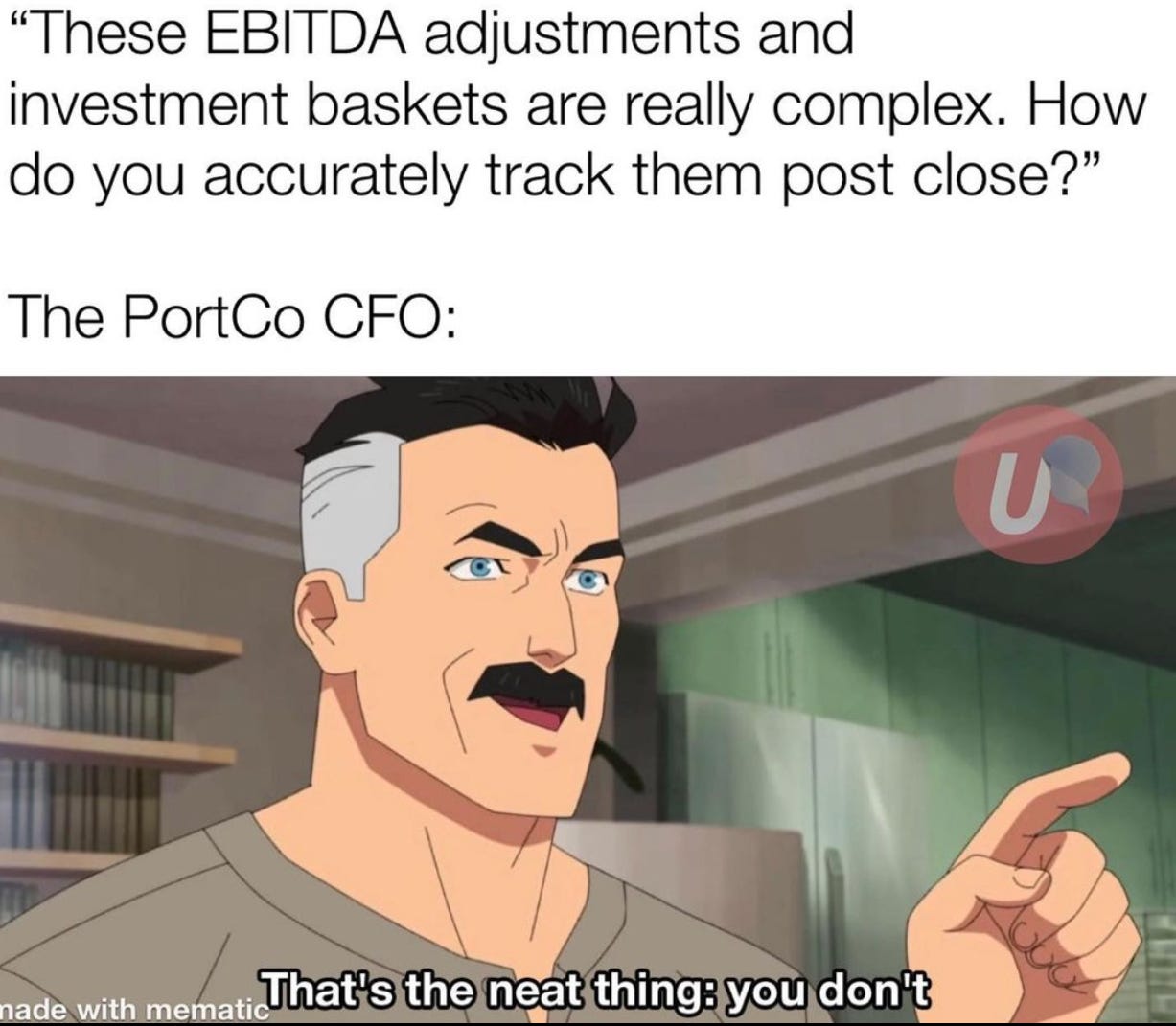

Available Amount: Unlike most of the other terms, which have a defined application/purpose, The available amount basket is a swiss army knife that can be used to pay out restricted payments (if borrower is above set incurrence test) as well as certain other investment baskets that would be otherwise restricted. The twisted (and somewhat fair) part about it is its fueled by the Company’s profits. The two components of this are referred to as the “starter” and the “builder”. The starter will be a fixed amount of EBITDA at close "(lets say 25% of EBITDA) and increases (the “builder”) in accordance with profits (known as “excess cash flow”) and cash proceeds from equity infusions and some types of divestitures. This nice little alley oop of credit agreement fuckery is fairly new to the leveraged loan market and trickled down from the high yield bond market (I think like ~10 years ago but don’t quote me on that). A little tangent, but the tracking / calculation of this thing is horribly inconsistent. I would say <20% of borrowers I’ve seen provide a tracker of the AA basket.

General Debt Basket: This is a fun little basket that allows for debt (stated as a % of closing EBITDA) to be incurred, with near unlimited potential for what kind of debt it can be. The crazy part of all these different debt baskets is that they can usually be stacked. So you could take your closing leverage (6.0x) + F&C bucket (1.0x) + general debt basket (0.5x) = 7.5x leverage when you only think the Company can afford to pay interest at 6.0x.

MFN (“most favored nations”): While not really a basket like the rest of these, I did a lil MFN meme drop the other day so wanted to cover it quickly. MFN is meant to keep existing lenders from getting screwed on economics if a borrower issues a new piece of debt that is higher priced than the current deal. So if MFN is 50bps and the current deal is S+600, any new incremental piece of debt that is S+750 or higher would “trigger” MFN. As a result, the existing debt would increase to be within 50 bps of the new piece of debt. Of course, there are usually tons of carveouts with this (related mainly to size and seniority of the new debt) that nefarious lawyers can sometimes use to avoid increasing existing pricing. Also some of the more borrower friendly deals have an MFN sunset, which eliminates the MFN provision after a certain amount of times (6 months - 18 months). A new more expensive tranche can send the existing debt’s open market treading price to the shadow realm (especially if MFN has expired), because there’s no reason to buy the cheaper debt now.

That’s it for today. Doing away with Q&A / inside baseball segments on this given its a longer one. Peace!